Second Half Crypto Market Narrative Trends

Looking at today's market, the narratives attracting capital and attention are quite clear. As Benjamin Graham said, "In the short run, the market is a voting machine, but in the long run, it is a weighing machine." We're currently in the 'voting' phase where narratives drive prices, but fundamentals ultimately determine weight. Today, let's analyze the current crypto market situation from both 'voting' and 'weighing' perspectives.

The Rise of DAT - Network Effects and Trust Premium

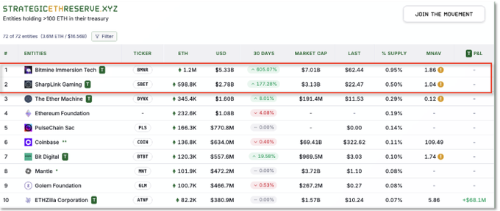

One major trend is DAT (Digital Asset Treasury companies) - essentially funds, companies, or ETFs that hold cryptocurrencies. Prime examples include Grayscale trusts and MicroStrategy, which served as Bitcoin 'proxies.' Successful DATs trade at premiums above their net asset value (NAV) - pricing created by network effects and 'trust,' not mere speculation.

For Bitcoin, Michael Saylor played this role. His reputation from the dot-com era and extensive public market experience translated to investor trust, making MicroStrategy stock surge as a Bitcoin proxy. For Ethereum, key figures include Joe Lubin (ConsenSys CEO) and Tom Lee. Lubin built bridges between traditional finance and Ethereum, while Lee gained public trust by analyzing Bitcoin on CNBC from early days. This background helped ETH reach 5-year highs in August 2025 amid corporate treasury buying and record ETF inflows.

Conversely, altcoin-based DATs face different circumstances. They often lack 'marquee figures' or brands that the public trusts, with network effects not extending to mainstream finance. This causes Sui token trusts or obscure alt ETFs to struggle with demand. Surviving this structure requires more than popularity within crypto communities - you need market-wide recognized leadership and institutional support for premiums.

Ultimately, the ETF/DAT narrative is about 'whose trust backs it.' Currently, Bitcoin and Ethereum own this stage while alts still wait in long lines for entry tickets.

Why Are Altcoins Pursuing DAT and Buybacks Now?

Recent altcoin markets show increased DAT issuance and buyback strategies. While appearing like simple 'price defense,' deeper fundamental reasons exist.

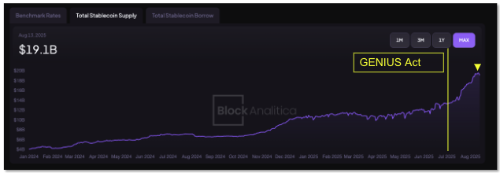

1) Narrative Exhaustion and Capital Flow ChangesOver the past year, global big tech and financial companies - Tether, Circle, Stripe - launched their own chains and payment networks, shifting market leadership. The US GENIUS Act (federal stablecoin regulation) accelerated institutional entry. Consequently, market premiums shifted from 'new L1s' to 'stablecoins/payments.' Post-legislation, stablecoin market cap has risen sharply.

In this environment, new altcoins and mid-tier projects struggle to push 'unique narratives.' They're pivoting toward fundamentals - actual revenue and value return - to convince investors.

2) Aggressive Buybacks and BurnsThis appears distinctly in DeFi protocols. Those generating solid revenue from trading fees or lending interest use profits for direct token buybacks/burns or dividend-like returns rather than diluting through incentive token printing. The approach: "If narratives can't sustain us, directly support prices."

3) Ethereum Ecosystem's Favorable ConditionsEthereum remains the center of high-fee, high-volume DeFi with institution-friendly regulatory environment. Post-merge scalability upgrades, ETF approval, and expanded on-chain finance weight solidified 'institution-ready' perception. GENIUS Act clarified stablecoin regulation, creating justification for institutional capital in on-chain yield products. Ethereum-based DeFi protocols doing aggressive buybacks can simultaneously capture DeFi, ETH, and real yield narratives.

4) Flywheel MechanismMany projects target simple dynamics: Low circulating supply + Real revenue → Buybacks → Price support → New investor inflow → More revenue → More buybacks. This maximizes when combined with compelling narratives. Conversely, projects without attractive stories or revenue returns face capital flight and stagnation. This explains recent struggles of some Layer 2s and AI tokens.

DeFi Revival - Stablecoin Yields and Institutional Inflows

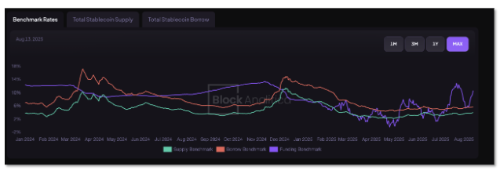

The most powerful catalyst reviving DeFi over the past year was the stablecoin sector. Stablecoins evolved from basic liquidity assets to 'yield-generating dollars.'

The first change was regulatory paradox. July 2025's US GENIUS Act prevented regulated stablecoin issuers from paying users interest directly. While CeFi interest accounts seemed to disappear, this created explosive demand for DeFi yields. Potentially trillions in stablecoins from institutions and large holders began seeking 'yield-paying venues.' If USDC or USDT can't pay interest directly, capital must flow to on-chain strategies. CoinFund's Chris Perkins' 'capital flow to DeFi yield vaults' became reality, rapidly growing protocols accepting stablecoin deposits.

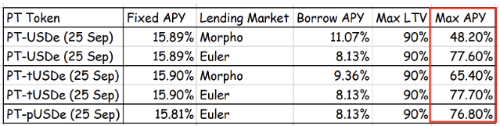

The second change was self-yielding stablecoins. Ethena's USDe exemplifies this - a dollar-pegged asset using spot long/futures short delta-neutral strategies for stable returns. Reaching $10 billion TVL in 500 days, it became history's fastest-growing stablecoin. This timing coincided with post-GENIUS Act period, growing through '8%+ high yields' that regulated dollar stables couldn't provide.

Sky Protocol (formerly MakerDAO) joined this trend, raising DAI Savings Rate (DSR) to 8% based on RWA investment returns. Stablecoins became productive assets, not 'just parked money.'

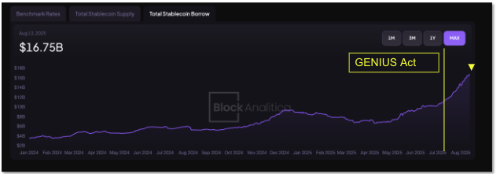

This change rests on mature infrastructure. On-chain lending markets absorbed large deposits from institutions and whales seeking safe yields, with stablecoin lending supply surging post-mid-2025. Some estimates suggest over $10 billion additional stablecoins were deposited in lending protocols since June. This liquidity kept DeFi lending rates moderately rising while stably supporting traders and leverage demand needing stablecoins.

Coinbase's On-Chain Expansion

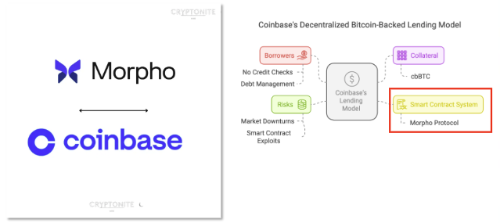

One of the most notable trends in the recent market is that fintech companies and major exchanges have begun seriously entering on-chain finance. Coinbase leads this charge. They didn't just create their own chain (Base) and stop there - they're now naturally integrating DeFi protocols into their services.

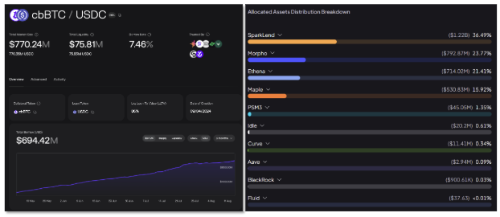

A prime example is their new lending product. When users deposit Bitcoin (cbBTC) with Coinbase, internally it goes through the Morpho protocol on the Base chain to borrow USDC. But from the user's perspective, this process looks as simple as clicking a few buttons on the exchange interface. The complex DeFi routing happens behind the scenes while the user experience is cleanly packaged.

This model is powerful because it hides DeFi's complexity while preserving its benefits. Users can naturally access on-chain yields without knowing about self-custody or MetaMask. From the exchange's perspective, traditional trading business is already a red ocean. It's difficult to profit from fee competition alone, so the next growth area must be on-chain finance. Coinbase is already reflecting transaction fees generated on the Base chain in their earnings, and growth potential expands significantly as more capital flows into lending, borrowing, and trading.

This isn't just Coinbase's story. Fintech companies like Robinhood and PayPal are likely to offer on-chain services like stablecoin yield products and tokenized asset trading to millions of users. What matters is "which protocols get selected for these partnerships."

For example, Morpho is expanding its institutional bridge role by connecting with Coinbase wallet. As Coinbase channels users and capital to Morpho, which has technology to boost supplier yields, network effects naturally accumulate. The same goes for Aerodrome, Base's native DEX. It attracted massive TVL from launch, and another wave of growth will come when Coinbase pushes DeFi to retail users.

Interestingly, Sky Protocol's (formerly MakerDAO) lending protocol Spark is supplying stablecoins to platforms like Morpho. This shows on-chain capital supply and demand becoming increasingly interconnected.

Coinbase's strategy delivers a simple message: ultimately, 'experience' and 'distribution' determine the game. Expecting all users to evolve into DeFi experts is unrealistic. The winning model embeds DeFi where users already are - exchanges and wallets. For protocols to capture this major integration trend, technical capability alone isn't enough. Those prepared with compliance, API completeness, and deep liquidity will be chosen.

We're witnessing CeFi and DeFi convergence. As this boundary collapses, crypto market narratives expand, and the distinction between 'crypto investors' and 'yield-seeking capital' increasingly disappears. In this context, BTCfi initiatives like Bitcoin Layer 2s and sidechains will likely lose momentum.

RWA - On-Chain Meets Off-Chain Finance

One of this year's major narratives is undoubtedly RWA (Real World Asset tokenization). This trend actually began in 2023 when massive players like BlackRock launched tokenized money market funds and brought US Treasuries on-chain, securing first-mover advantage. But 2025 changed the game. It's no longer about "who does it first" but "who can most effectively utilize RWA."

@ventuals_

RWA is used in DeFi in two main ways. First is yield - bringing real yield assets like Treasuries and credit on-chain to back stablecoins or provide lending rates. Second is trading - making tokenized stocks, funds, and even pre-IPO shares tradable 24/7 on-chain. This extends to sports/event betting markets and prediction markets. If retail traders worldwide could long/short pre-IPO company tokens or easily do leveraged betting on-chain that's difficult in traditional finance, it could absorb massive speculative demand. These attempts are still early stage, but they could be crucial points for expanding the DeFi market beyond simple yield narratives.

Most importantly, RWA is no longer just a 'buzzword' - it's generating real cash flows. For example, SKY (MakerDAO) expects about $250 million annual revenue from RWA assets, while Maple Finance rapidly grows its loan book by providing institutional loans to Bitcoin miners and financial institutions.

Notably, S&P Global has started rating DeFi protocols. SKY received one of the first credit ratings, though it was sub-investment grade by traditional finance standards. The point is DeFi increasing touchpoints with traditional finance.

Future RWA competition won't be about 'who does it first' but 'who can scale stably and continuously supply liquidity.' The market already rewards projects like SKY and Maple Finance that show execution and traction. Surviving this narrative depends on safely and regulation-friendly connecting on-chain efficiency with off-chain assets.

Ethereum's Next Chapter - Scalability and Privacy

Ethereum remains the center of digital assets. But to maintain that position, it must continue evolving. The two most prominent keywords in Ethereum's current roadmap are scalability and privacy.

Starting with scalability, Vitalik Buterin recently made a quite radical proposal: long-term abandonment of EVM for RISC-V based zkVM. RISC-V is a modern processor architecture that, combined with zero-knowledge proofs, could increase L1 throughput 50-100x over current levels. Rather than relying solely on rollups, this would 'supercharge' L1 by upgrading the base engine itself. Teams like Risc0, Jolt, and Polygon Miden are already researching this direction. If realized, the "L1 scaling narrative" that seemed dead could revive.

Next is privacy. For institutions, privacy is closer to necessity than choice. What happens when a hedge fund opens a hundred-million-dollar position on a completely transparent chain? It immediately becomes a target for front-running or copy trading. As a Galaxy Digital trader said, "Privacy isn't a simple regulatory checkbox but a survival condition for protecting on-chain trading strategies."

Several approaches are being researched simultaneously:

ZK Rollup variants: Models like Aztec and StarkNet that encrypt transaction data while proving validity

Layer privacy tools: zk-SNARK based systems like Railgun, which gained attention when Vitalik used it directly and is seeing increasing usage

Hybrid networks: Consortium chain models like Canton Network backed by Deloitte, where transactions are visible only to necessary parties while others are blind

While Ethereum itself won't implement full privacy at L1, possibilities remain open through L2s or new VM structures. The RISC-V zkVM push is particularly meaningful as it makes ZK computation cheaper, ultimately enabling private transactions everywhere.

Looking ahead, institutions could conduct completely confidential transactions on Ethereum or connected networks, with only regulators or approved counterparties seeing transaction details. This would open doors to on-chain FX, securities, and derivatives.

In summary, Ethereum is moving toward becoming a "high-performance + privacy" global settlement layer. While this theme may not look flashy to retail investors immediately, it profoundly impacts ETH's long-term value. This change connects to opportunities for specific projects. ZK variants like zkSync, StarkNet, and Polygon zkEVM, plus distributed validator infrastructure like Obol, are likely puzzle pieces.